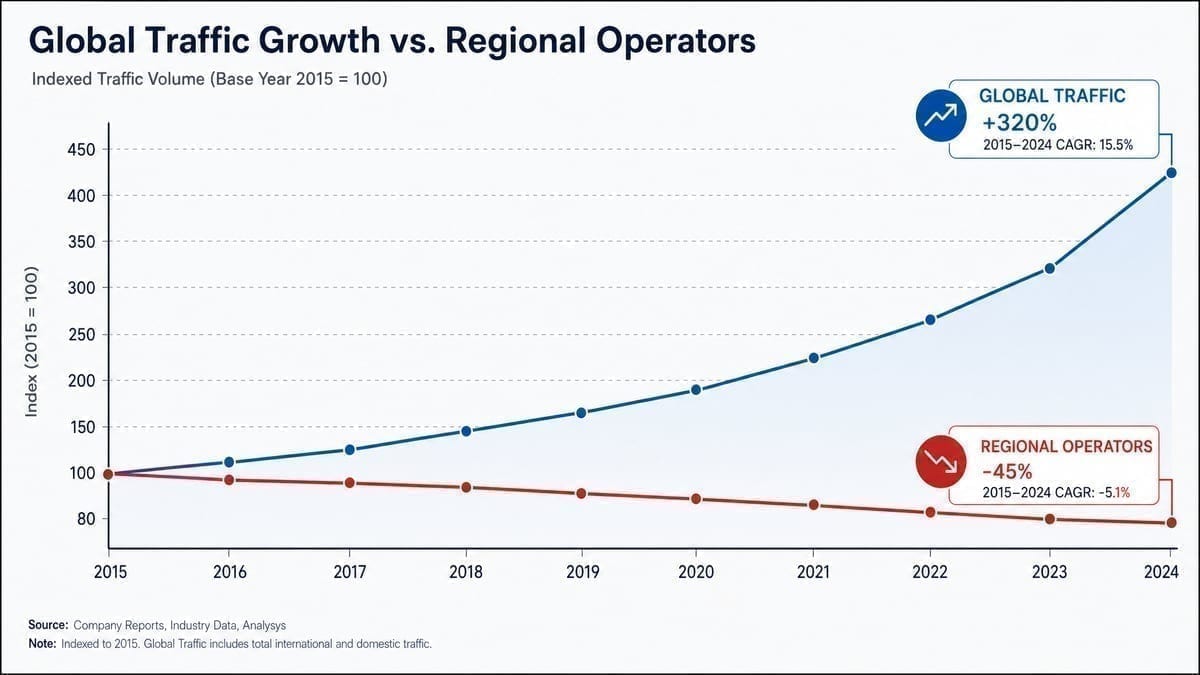

The poker industry just witnessed something unprecedented. GGPoker hit 900,000 concurrent players. PokerStars dropped a $50 million anniversary guarantee. Traffic records fell like dominoes across every major international operator.

But dig into state-by-state revenue reports and operator earnings calls, and you’ll find a starkly different narrative playing out in regional markets. The same week GGPoker celebrated its traffic milestone, three mid-tier US operators quietly reduced guarantees. Two European sites merged player pools just to keep cash games running. A once-thriving Asian network shut down entirely.

The global poker boom is real. So is the regional poker bust. And they’re happening simultaneously.

The Two-Speed Poker Economy

Think of it like the airline industry after deregulation. The mega-carriers got bigger, flying more passengers than ever on increasingly profitable international routes. Meanwhile, dozens of regional airlines went bankrupt trying to compete on thin-margin domestic flights.

That’s poker in 2026.

Global sites operate like network airlines - they connect players from London to São Paulo to Manila in massive tournaments with life-changing prizes. Their rake per player might be lower, but when you’re dealing millions of hands per hour across time zones, the economics work brilliantly. GGPoker’s recent $300 million guarantee for their World Festival wasn’t hubris. It was a calculated bet on network effects.

Regional operators face the opposite dynamic. Limited to single states or small countries, they’re fighting over player pools that haven’t grown since launch. Pennsylvania’s April revenue hit records - but that’s because BetMGM and BetRivers split PokerStars’ former monopoly, not because more Pennsylvanians suddenly started playing online poker.

Why Market Share Metrics Lie

Here’s where it gets tricky for investors and analysts. Traditional market share calculations make regional operators look healthier than they are.

When BetMGM claims 50% market share in New Jersey, that sounds impressive. But 50% of a $3 million monthly market barely covers operational costs. Their poker platform requires the same development resources, support staff, and marketing budget as a site generating 20 times the revenue. The math simply doesn’t work long-term.

888poker learned this lesson painfully. Their recent XL Spring RakeLESS Main Event headed for a massive overlay because even removing rake entirely couldn’t attract enough players to meet guarantees. When free money can’t fill your tournaments, you have a fundamental liquidity problem.

The consolidation has already started. FanDuel absorbed PokerStars in North America. Smaller operators will follow - not because they want to sell, but because they can’t afford not to.

The Technology Gap Widens

Software development costs follow a power law distribution. Building a basic poker client costs X. Making it competitive costs 10X. Creating something that can challenge GGPoker or PokerStars costs 100X.

Regional sites can’t spread those development costs across enough players. So they make compromises. Fewer game variants. Delayed mobile updates. Minimal innovation.

Players notice. And they migrate.

GGPoker’s recent UI overhaul might have sparked complaints about eye strain, but at least they’re iterating. Their Rush & Cash format, Smart HUD integration, and built-in staking platform required serious investment. Regional sites counter with… bigger deposit bonuses. It’s bringing a knife to a gunfight.

This technology gap creates a vicious cycle. Fewer features mean fewer players. Fewer players mean less revenue for development. Less development means falling further behind. Eventually, the platform becomes uncompetitive regardless of promotions or rakeback offers.

What This Means for Players

The implications differ dramatically based on where you play.

If you’re grinding on global sites, enjoy the golden age. Tournament guarantees will keep climbing as operators compete for recreational players. New features will roll out monthly. The games might get tougher as [weak sites die and their regs relocate, but overall liquidity ensures action around the clock.

Regional players face tougher choices. Your site might offer 50% rakeback and daily freerolls, but can it survive another year? Banking your entire bankroll on a struggling operator carries real risk - not of theft, but of waking up to a “ceased operations” notice.

Smart players are diversifying. Keep some action on regional sites for soft games and promotions, but maintain accounts on stable platforms too. Think of it as portfolio management for your poker career.

The Endgame

Consolidation in mature industries follows predictable patterns. Many competitors enter during the growth phase. Most fail or merge during maturity. A handful of giants dominate the stable phase.

Poker already passed through growth. We’re deep into the consolidation phase now.

Within five years, expect three to five global operators controlling 80% of worldwide poker liquidity. Regional markets will have one, maybe two viable sites each. Everyone else becomes a skin, an acquisition target, or a cautionary tale.

For the winners, the economics look fantastic. GGPoker proved you can be hugely profitable while offering reasonable rake and massive guarantees - if you have scale. For losers, the exit might not even cover their marketing spend from the glory days.

The house always wins in poker. But increasingly, only the biggest houses can afford to stay in the game.